CoreWeave IPO - Why it is Risky!

Breaking out reasons why I would not touch it - my goals are not yours

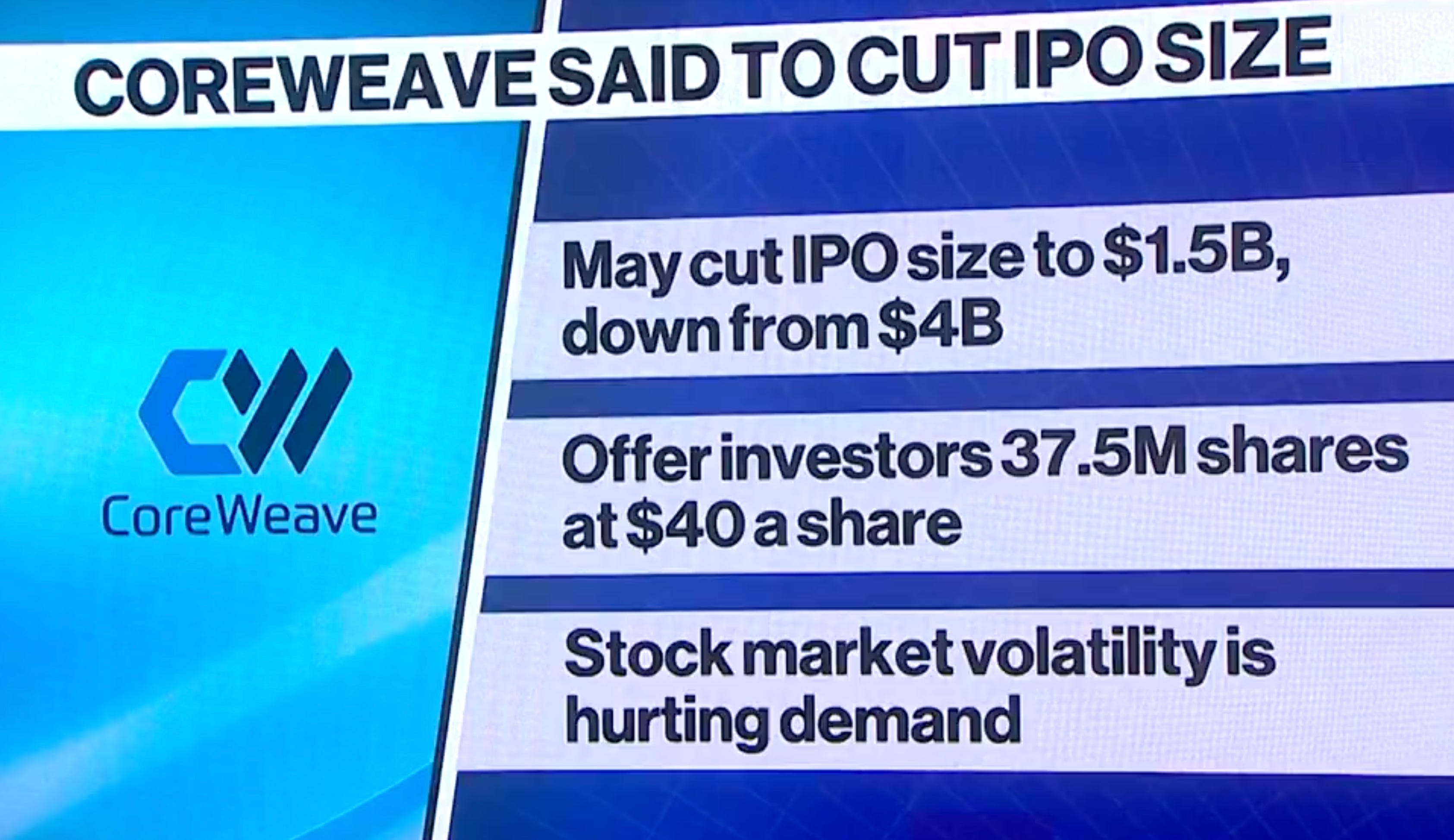

Coreweave IPO Tomorrow

Lot's of Q's of should I buy the Corewave IPO tomorrow... as usual of course not!. Let me explain why.

CoreWeave, an AI hyperscaler originally founded in 2017 as a crypto mining outfit, raised $1.5 billion in a downsized initial public offering (IPO) on March 27, 2025, as reported by Bloomberg. The New Jersey-based company sold 37.5 million shares at $40 each, falling short of its earlier ambitions to raise $2.69 billion (49 million shares at $47–$55) or even $4 billion at a $35 billion valuation.

Why I believe CoreWeave's stock debut is expected to be rocky:

Downsized IPO Reflects Weak Market Confidence ie raised only $1.5 billion against a $4 billion target, with shares sold at $40 instead of the planned $47–$55 range

Heavy Customer Concentration Risk - 77% of revenue comes from just two clients (Microsoft at 62% alone) and they are scaling back Data Center Contracts.

Monstrous Debt - $13 billion in debt, largely tied to GPU-backed lending and we know how fast those puppies depreciate. Oh at hi rates also.

Corewave fit a temporary gap in AI compute capacity, but this edge will vanish as competitors scale up

Fierce Competition - hyperscalers like Microsoft, Amazon, and Meta, who plan $340 billion in 2025 capex and even Bitcoin miners who are ruthless and many have not figured out to turn a dime on Bitcoin Mining.

ZERO PROFITS - Reported an $863 million net loss in 2024 despite 700% revenue growth to $1.9 billion.

Rem with most IPOs the insiders and Banksters already got theirs, time to bring Retail to the slaughter.